In Accounting For A Defined-benefit Pension Plan

4-step accounting for defined benefit plans under IFRS Step 1. Determine the present value of the defined benefit obligation by applying an actuarial valuation method The ultimate cost of a defined benefit plan is uncertain and is influenced by variables such as final salaries employee turnover and mortality employee contributions and medical cost trends.

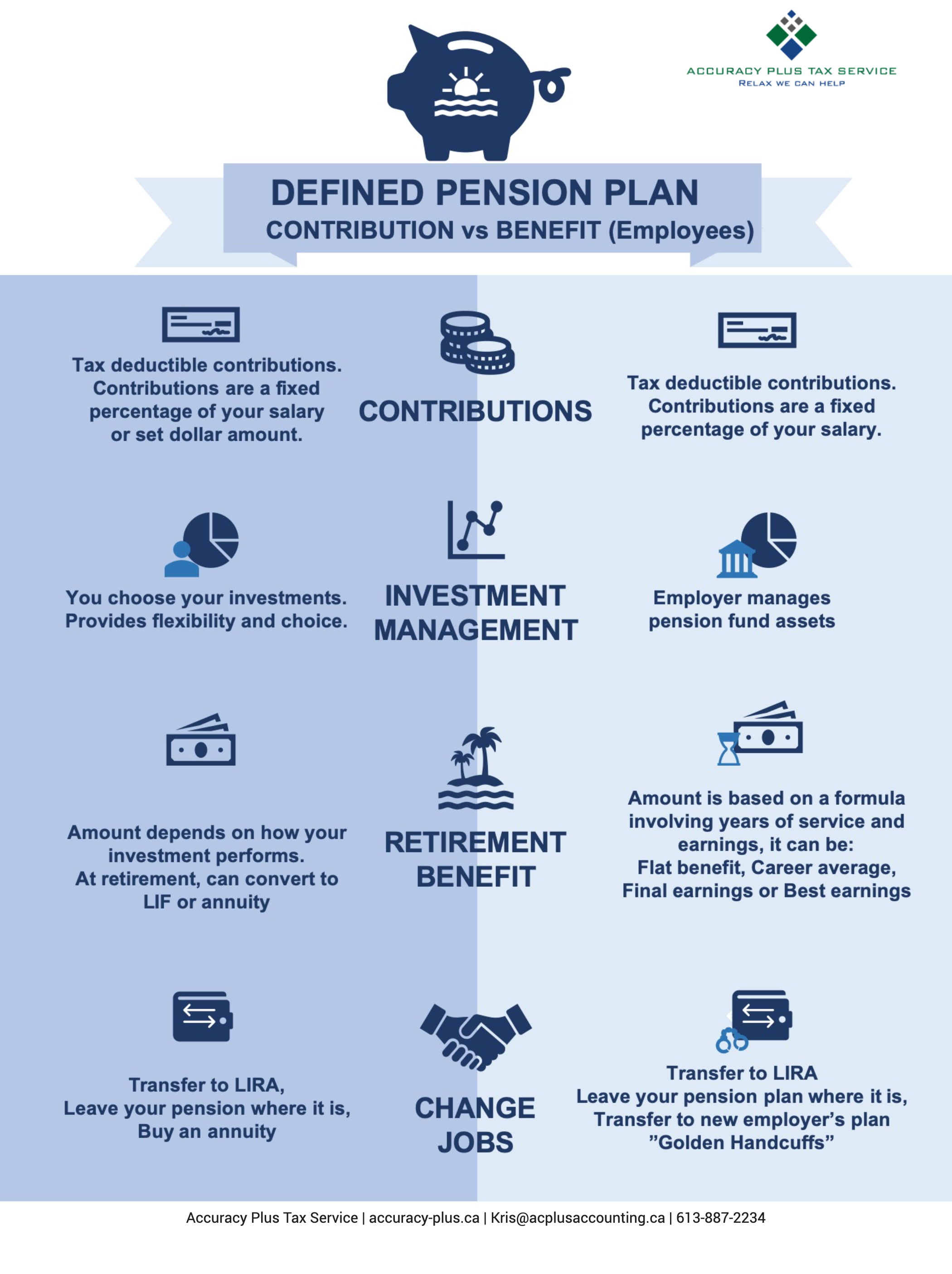

Defined Contribution Vs Benefit Pension Plan For Employees Accuracy Plus Tax And Services

The employers responsibility is simply to make a contribution each year based on the formula established in the plan.

In accounting for a defined-benefit pension plan. Prior Pension Accounting Standards Many organizations that sponsor a defined benefit pension plan have a significant portion of their balance sheet and income statement tied to and influenced by the volatility of pension liabilities and assets. Accounting For Pensions Defined Benefit vs. Certain components of pension expense may be reported as a part of different line items in the income statement B.

Employee benefits and IAS 26. Since there are usually many individual plan members an organization is typically formed to represent all of them collectively as a plan sponsor eg. 2017-06Investments in master trusts are presente d in a.

In March 2017 the FASB issued ASU 2017-07 which amends the requirements in ASC 715 related to the income statement presentation of the components of net periodic benefit cost for an entitys sponsored defined benefit pension and other postretirement plans. Defined benefit plan Company pays out benefits on retirement eg. This alert provides background on the traditional.

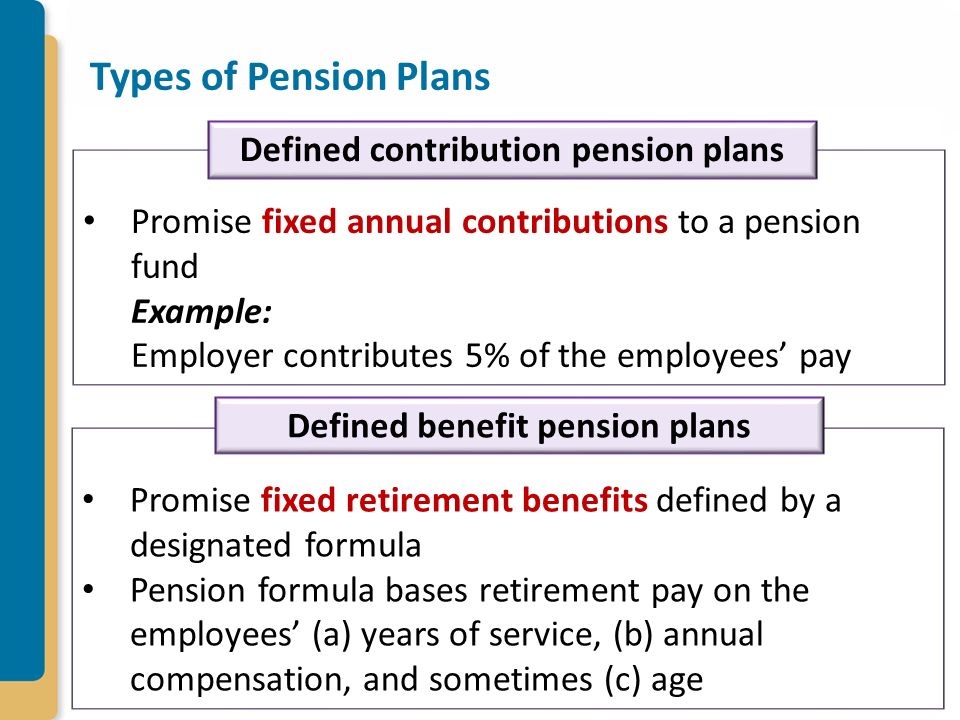

Typical private sector retirement pension plans Defined Contribution Plan. Under defined benefit pensions accounting universities are required to report the following items calculated by an actuary using the approach specified in FRS 102. Thats why Heather Horn and PwC pension specialist Nicole Berman go back to the basics to highlight a few of the fundamental accounting rules for these types of plans including.

Basic elements of pension accounting 2. Plan AccountingDefined Contribution Pension Plans Receivables Subsequent Measurement Participant Loans 962-310-35-2 Participant loans shall be measured at their unpaid principal balance plus any accrued but unpaid interest. Liabilities and assets 4.

Employers often need to develop models to predict future payout scenarios which depend on demographic factors interest rates inflation rates etc. Any portion of prior service cost that is not. During the year the firm earned 15 on its assets and made an additional contribution of 25000 to the plan.

233 - Remeasurement. Both employers and employees can pay into defined contribution plans. Accounting for Defined Benefit Plans.

GAAP in all of the following areas except that under IFRS A. There exist comprehensive requirements for the reporting of. GAAP net benefit cost ie defined benefit pension cost and postretirement benefit cost consists of several.

Defined Contribution Plans. Balance Sheet will contain prepayments asset or accruals liability to account for timing mismatch between cash contributions and income statement expenses. Value the net asset or liability position of the pension plan on a fair value basis.

Employee benefits under new UK GAAP FRS 17. Accounting for defined benefit pension plans can be a complex area and companies need to be aware of the guidance. The SEC staff recently met with representatives of the Big Four accounting firms and expressed its views on applying an alternative approach for using discount rates to measure the components of net periodic benefit cost for a defined benefit retirement plan obligation eg a pension or other postretirement obligation under ASC 715.

A defined contribution plan is a pension plan in which the employer is responsible only to the extent of its contributions and the risks are all borne by the employees. An International Comparison of Exchange-Listed Companies Defined benefit pension plans can entail one of the biggest liabilities that an exchange-listed company has on its balance-sheet. Accounting and reporting by retirement benefit plans.

Accounting for the long-term nature of these liabilities has always been complex. Retirement benefits IAS 19. The pensions accounting treatment for defined benefit plans requires.

The monies paid in serve to build up a fund that can be used to provide an income on retirement usually by means of an annuity. Accounting for a defined benefit plan. The Types of Pension Costs.

Net periodic pension cost 3. Determine the amount of pension expense for the year to be reported on the income statement. Pension contributions payable are expensed to P.

The first statement known as SORP 1 was published by the Accounting Standards Committee in 1986 and was based on the 1978 report. The expected benefit payments under a defined benefit plan are subject to significant actuarial assumptions. The employer recognizes contributions due as an expense and records any prepaid or accrued contributions on balance sheet.

Determine the fair value of the assets and liabilities of the pension plan at the end of the year. Net pension asset or liability on the balance sheet the difference between the pension scheme assets and liabilities at the reporting date. Costs and obligations 5.

A jointly sponsored pension plan is a defined-benefit plan in which an employer shares risks and rewards in the plan equally with the plan members who are current employees and retirees. We also have separate resources on FRS 102. In essence the accounting for defined benefit plans revolves around the estimation of the future payments to be made and recognizing the related expense in the periods in which employees are rendering the services that qualify them to receive payments in the future under the terms of the plan.

Plan AccountingDefined Benefit Pension PlansNet Assets Available for Plan Benefits Other Presentation Matters Investments in Master Trusts 960-30-45-11 Paragraph superseded by Accounting Standards Update No. Assume that at 1100 the pension plan had assets of 200000 and an expected rate of return of 10. In accounting for a defined-benefit pension plan a.

Actuarial gains and losses may be recognized in full in the period in which they occur directly into equity C. Statements of Recommended Practice. Accounting principles for defined benefit pension plans under IFRS differ from US.

Add paragraph 962-310-45-2 and its related heading with a link to transition paragraph 962-310-65-1 as follows. In a defined benefit pension plan the benefits are known defined and guaranteed and the contributions will vary depending on the amount needed to fund the defined benefits.

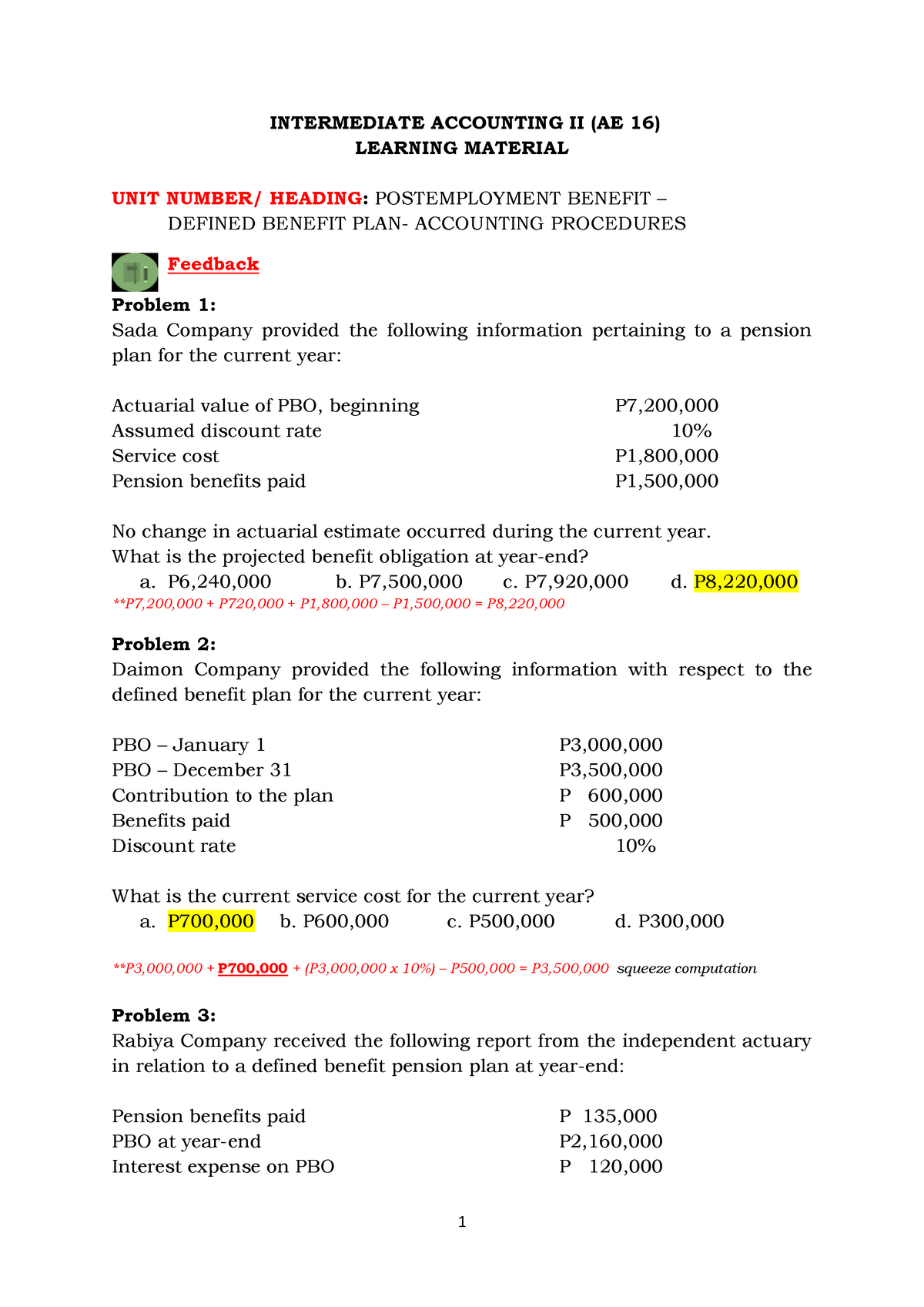

Defined Benefit Plan Exercises With Answers 1 Intermediate Accounting Ii Ae 16 Learning Studocu

Making Pension Adjustments Amt Training

/GM_Pension-2b3a5e03ee184c1a86e75a9ac4ebf2fd.png)

Projected Benefit Obligation Pbo Definition

Postretirement Benefits Ppt Download

Postretirement Benefits Ppt Download

How To Calculate Pension Expense For A Defined Benefit Plan Youtube

2021 Cfa Level Ii Exam Cfa Study Preparation

Ifrs Vs Gaap Accounting Amt Training

Defined Benefit Plan Exercises With Answers 1 Intermediate Accounting Ii Ae 16 Learning Studocu

Ifrs Vs Gaap Accounting Amt Training

Postretirement Benefits Ppt Download

Ifrs Vs Gaap Accounting Amt Training

/GM_Pension-2b3a5e03ee184c1a86e75a9ac4ebf2fd.png)

Projected Benefit Obligation Pbo Definition

Defined Benefit Vs Defined Contribution Pension Plan Youtube

{kind=link}

Posting Komentar untuk "In Accounting For A Defined-benefit Pension Plan"