Accounting 605 Vs 606

ASC 606 requires more comprehensive and detailed disclosures than what is currently required under ASC 605. Indicators of Gross Reporting.

Six System Objectives For Meeting The New Rev Rec Standards Ndh

The table below summarizes key differences between ASC 605-35 and ASC 606 regarding long-term contracts in the AD industry.

Accounting 605 vs 606. Contracts can be written oral or implied by an entitys customary business practices. Enforceability of the rights and obligations in a contract is a matter of law. What is ASC 606.

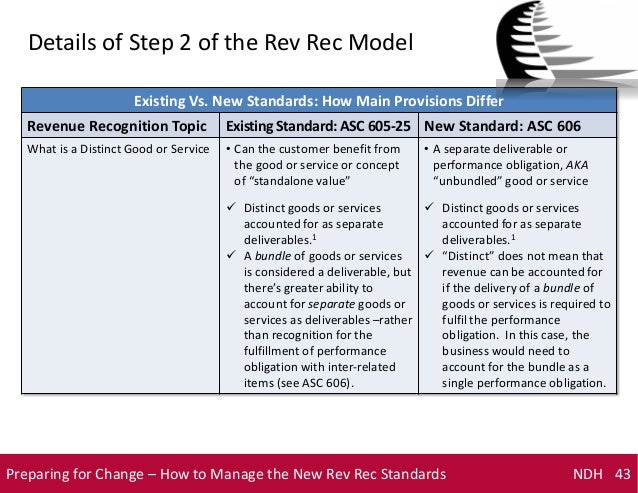

Key Differences Between ASC 605-35 Formerly SOP 81-1 and ASC 606. PHASE 2 - TECHNICAL ANALYSIS. The construction company can make an election for an output method units produced estimated completion or an input method incurred costs labor hours used.

According to ASC Topic 606 a contract is an agreement between two or more parties that creates enforceable rights and obligations. ASC 606 is effective for non-public companies for fiscal years beginning after December 15 2018. ASC 605-45 lists several indicators to help companies perform gross versus net reporting analysis for each revenue stream.

1 and codified in ASC 606 by the FASB and as IFRS 15. ASC 605-35 Formerly SOP 81-1 ASC 606. This is important because companies may have to assess the scope of both ASC 606 and ASC 808 for these types of arrangements.

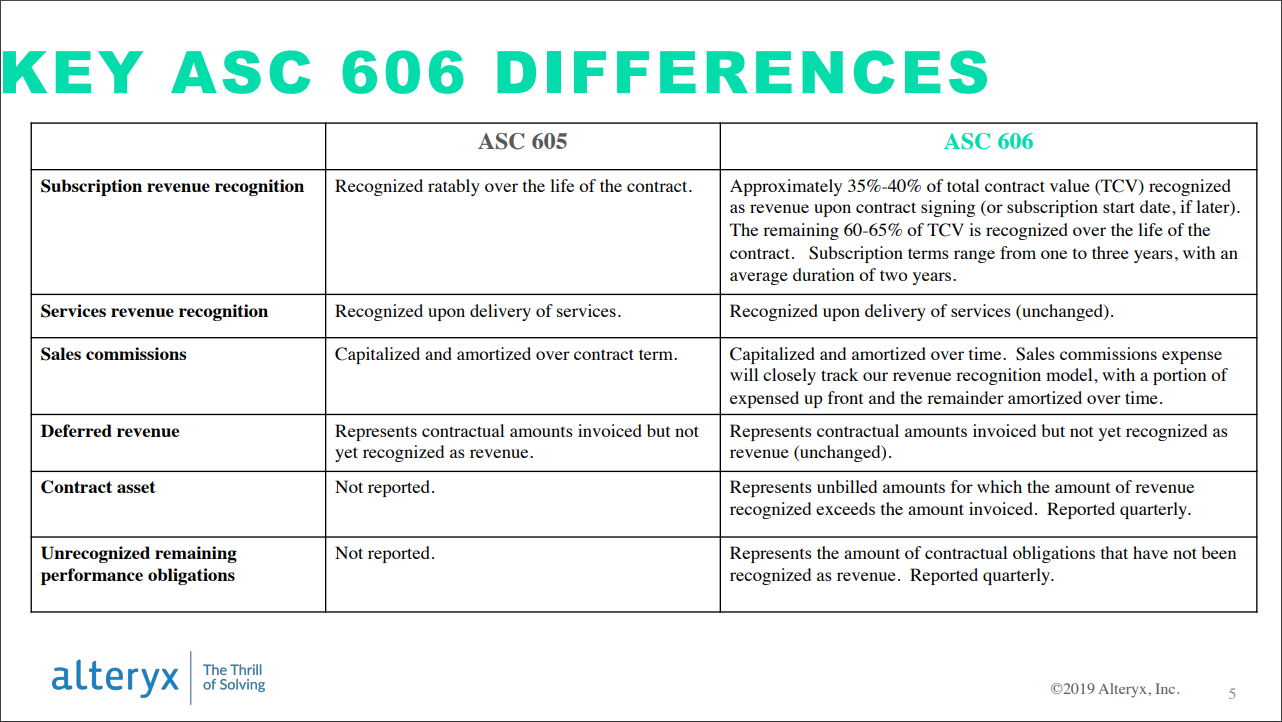

The standard issued as ASU 2014-09. Options for calculating percent complete are very similar between the old ASC 605 and the newer ASC 606. Under 605 these variable revenues were only booked when recognized.

Under 606 these variable revenues need to be estimated over the service-subscription life. The Bottom Line In May 2014 the FASB and the International Accounting Standards Board IASB issued their final standard on revenue from contracts with customers. It is an industry-neutral revenue recognition model designed to increase financial statement comparability among companies and industries.

ASC 606 for those revenue streamsaddressing. 2017-13 September 2017 Amendments to SEC Paragraphs Pursuant to the Staff Announcement at the July 20 2017 EITF Meeting and Rescission of Prior SEC Staff. For private companies now tasked with ASC 606 implementation the model supersedes most legacy guidance and fundamentally changes how entities need to think about revenue recognition.

ASC 606 will eliminate use of sell-through methods of revenue recognition for software sales. Rest of the in-depth answer is here. The Accounting Standard Codification 606 or ASC 606 made its debut in May 2014.

ASC 606 is the new revenue recognition standard that affects all businesses that enter into contracts with customers to transfer goods or services public private and non-profit entities. The objective is to decrease complexity involved with the current models for revenue recognition. It does not address all possible fact patterns and should be read in conjunction with ASU 2014-09.

Both public and privately held companies should be ASC 606. When selling through resellers and distributors some companies will wait to record actual revenue after price concessions and returns following sale to the end user. This is a bit of a paradigm shift in the FASBs approach to standard setting.

ASC 606 provides guidance when companies use a percentage-of-completion method. ASC 606 is a principle-based standard that provides construction financial managers with some subjectivity when assessing the standard. Prepare a gap analysis of ASC 605 vs.

Private company ASC 606 adoption. Under 606 these variable revenues need to be estimated over the service-subscription life. Determine specific application of issues identified in Phase 1 including method of determining standalone.

When choosing a method of reporting revenue one should be evaluating each indicator on a qualitative basis. Take an inventory of revenue streams identifying those to be impacted. During that service span there is usually variable revenue of some sort extra service costs usage-based or volume-based charges instead of flat rate charges.

Under ASC 606 you have to capitalize them. The entity is the primary obligator in the arrangement. Under 605 these variable revenues were only booked when recognized.

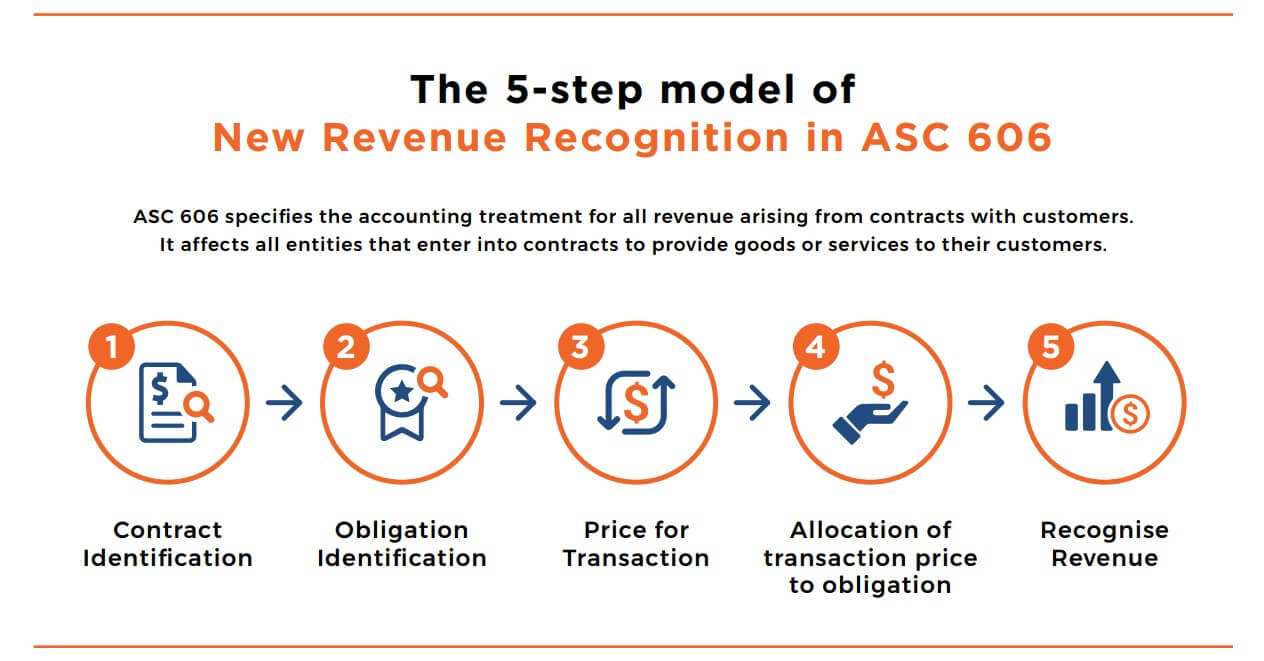

The new revenue recognition standard ASC 606 outlines a single comprehensive model for accounting for revenue from customer contracts. The new disclosure requirements aim to provide information that will make it easier for financial statements users to understand the nature amount timing and uncertainty of revenue and. Contract review considerations US2019-10 Most nonpublic companies will be required to adopt the new revenue standard in 2019.

The ASC 606 accounting standard replaced the previous ASC 605 and the main reason for the switch was a need to bring GAAP revenue recognition standards in the US to a better level of compliance with the IFRS International Financial Reporting Standards. As part of their implementation companies will need to review their contracts and assess the accounting. In addition the ASUs Basis for Conclusions does not preclude companies from analogizing to the guidance in ASC 606 when accounting for collaborative arrangement transactions within the scope of ASC 808.

An Amendment of the FASB Accounting Standards Codification Revenue Recognition Topic 605 Revenue from Contracts with Customers Topic 606 Leases Topic 840 and Leases Topic 842 No.

Asc 606 The New Revenue Recognition Standard Howlite Inc

Recognizing Software Revenue

Alteryx A Little Saas Accounting Lesson Nyse Ayx Seeking Alpha

Allocation Difference In Asc 606 Ifrs 15 Vs Ind As 18 Revgurus

Revenue Recognition Gaap Dynamics

Bnft Ex992 95 Pptx Htm

Sec Filing Gogo Inc

How Asc 606 Impacts Your Subscription Business Paykickstart

Practical Applications Of Asc 606 For Saas Companies Fei

New Revenue Recognition Standards Asc 606

2

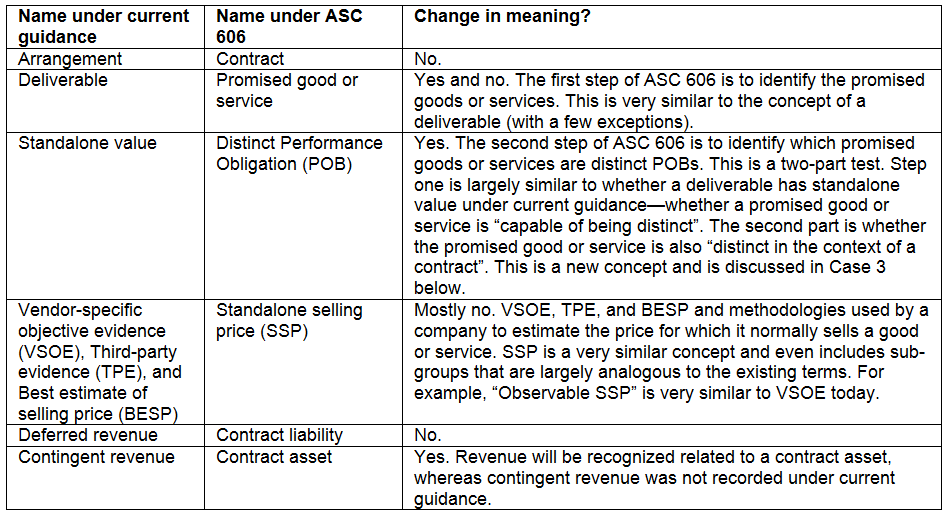

Asc 605 To 606 What S Changed Mike Sandrik

New Revenue Recognition What Does My Nonprofit Need To Know

Practical Applications Of Asc 606 For Saas Companies Zuora

{kind=link}

Posting Komentar untuk "Accounting 605 Vs 606"